Morgan Stanley

Corporate Credit 1Q 2022

FOR FINANCIAL ADVISORS ONLY. NOT FOR PUBLIC DISTRIBUTION.

Summary

U.S. corporate credit markets declined sharply in the first quarter amidst a large backup in interest rates as bank loans significantly outperformed high yield bonds and investment grade corporate bonds in the first quarter. Bank loans returned -0.10% during the period as measured by the Credit Suisse Leveraged Loan Index. High yield bonds faced their worst quarter since the first quarter of 2020 and returned -4.84% as measured by the Bloomberg U.S. Corporate High Yield Bond Index. Investment grade corporate bonds underperformed amidst a rout in longer duration assets and returned -7.69%, the worst quarterly return since 2008, as measured by the Bloomberg U.S. Corporate Bond Index.

U.S. equities fell as the S&P 500 Index returned -4.60% during the period. The decline was driven by several factors including an aggressive hawkish pivot from global central banks led by the Federal Reserve (Fed), persistent inflationary pressures and a spike in geopolitical tensions emerging from Russia’s invasion of Ukraine in February. U.S. economic data painted a mixed picture as the labor market continued to improve while inflation continued to rise. The unemployment rate fell to 3.8% in February, its lowest level since February 2020, while inflation accelerated further from already elevated levels as the February Consumer Price Index (CPI) rose by 7.9% year-over-year, the fastest annual pace in nearly 40 years. At its March meeting, the Fed voted to raise the target for the benchmark federal funds rate by 25 basis points, the first increase since 2018. The Fed reiterated additional interest rate hikes will be needed, and it will accelerate the pace of tapering, reducing its holdings of Treasuries, agency debt and agency mortgage-backed securities (MBS). Geopolitical tensions also rose significantly with Russia’s invasion of Ukraine, further clouding the global economic outlook and sparking a broad-based rally in commodities. On the COVID-19 front, while trends continued to improve in the U.S., a resurgence in China toward the end of the quarter led to regional lockdowns and added further uncertainty to the global growth outlook.

Market Environment

U.S. Treasury yields rose sharply in the first quarter with the front end of the curve leading the way, resulting in significant bear flattening. The yield on the U.S. 2-Year note climbed roughly 160 basis points during the period, while the yield on the U.S. 10-Year note rose roughly 83 basis points. The curve flattened further and threatened inversion beyond the 2-Year point toward the end of the quarter as the Treasury market rapidly repriced the Fed’s tightening cycle. Longer duration bonds underperformed as the Bloomberg U.S. Aggregate Bond Index fell 5.93%, its largest quarterly decline in more than 40 years.

Alongside the selloff in risk assets, corporate credit spreads widened modestly but ended the quarter well off their widest levels seen in early March. High yield bond spreads widened roughly 38 basis points but ended the quarter more than 80 basis points below the March high as measured by the Bloomberg U.S. Corporate High Yield Bond Index. Investment grade corporate bond spreads also widened roughly 22 basis points as measured by the Bloomberg U.S. Corporate Bond Index.

High yield bond issuance slowed markedly in the first quarter with issuance totaling roughly $43 billion, the lowest first quarter total since 2016, as borrowers were cautious amidst the market turmoil and sharp backup in yields. Investment grade corporate bond issuance topped $450 billion in the first quarter with issuance rebounding in March, as monthly supply topped $230 billion. Additionally, leveraged loan supply totaled close to $110 billion in the first quarter, a modest slowdown compared to last year’s pace.

On the demand side, investors continued to favor bank loan funds over high yield bond and investment grade corporate bond funds amidst robust demand for floating-rate instruments. U.S. leveraged loan funds experienced inflows of nearly $20 billion in the first quarter, while U.S. high yield bond funds experienced outflows of nearly $25 billion and investment grade corporate bond funds experienced outflows of more than $10 billion.

Within the high yield bond market, the riskier segments outperformed as ‘B’s (-3.53%) and ‘CCC’s (-3.88%) outperformed ‘BB’s (-5.94%) with higher quality bonds bearing more interest rate risk than the lower quality segments of the market. From an industry perspective, Energy (-2.60%) outperformed led by the rally in commodities, while Communications (-6.60%) trailed the broader high yield bond market. Default activity remained very low by historical standards with only $1.6 billion of actual defaults during the quarter as the 12-month trailing, par-weighted U.S. high-yield default rate fell to a record low of 0.23% at the end of March.

Performance and Attribution Summary

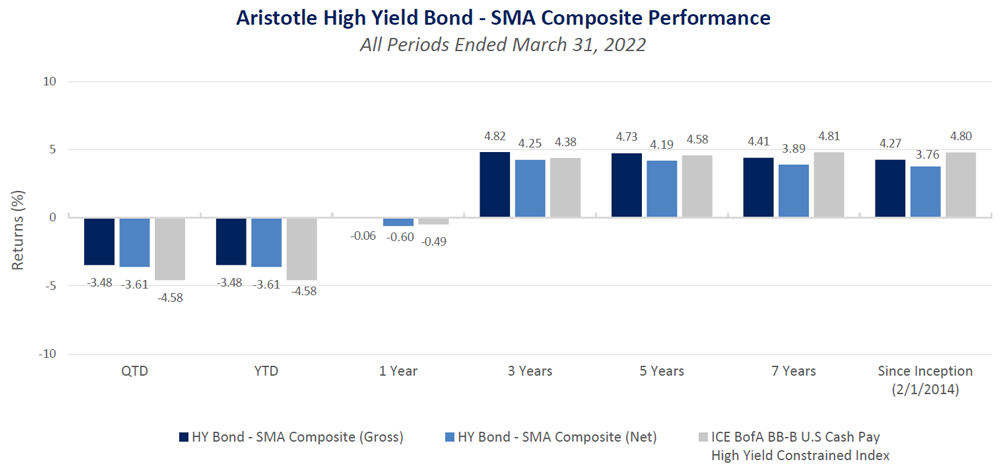

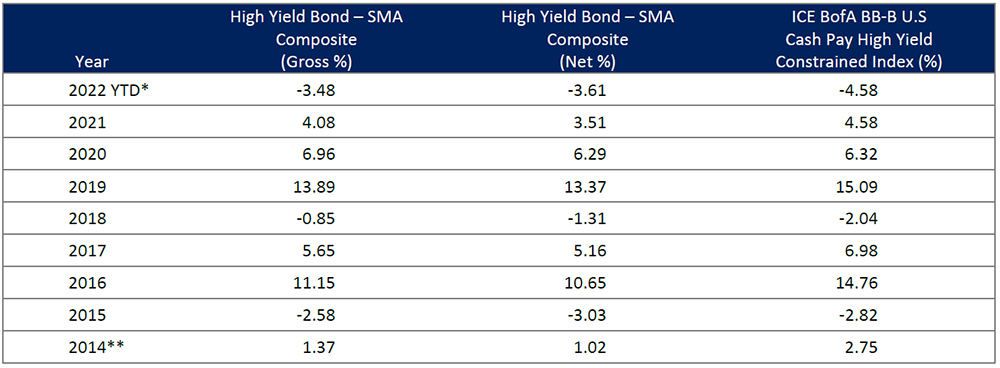

High Yield Bond – SMA

The Aristotle High Yield Bond – SMA Composite returned -3.48% gross of fees (-3.61% net of fees) in the first quarter, outperforming the -4.58% return of the ICE BofA BB-B U.S. Cash Pay High Yield Constrained Index.

Security selection contributed to relative performance led by holdings in Media & Entertainment and Automotive & Captive Finance. This was partially offset by security selection in Telecommunications and Diversified Manufacturing & Construction Machinery. Industry allocation also contributed to relative performance led by an underweight in Food, Beverage & Tobacco and an overweight in Media & Entertainment. This was partially offset by an underweight in Energy and an overweight in Automotive & Captive Finance. Additionally, sector rotation contributed modestly to relative performance led by the allocation to cash, which was partially offset by the allocation to investment grade corporate bonds.

| Top Five Contributors | Top Five Detractors |

|---|---|

| Quad/Graphics | PBF Energy |

| Kraft Heinz | Level 3 Financing |

| Tenneco | Dell |

| Murphy Oil | Telecom Italia |

| Mercer International | Airlease |

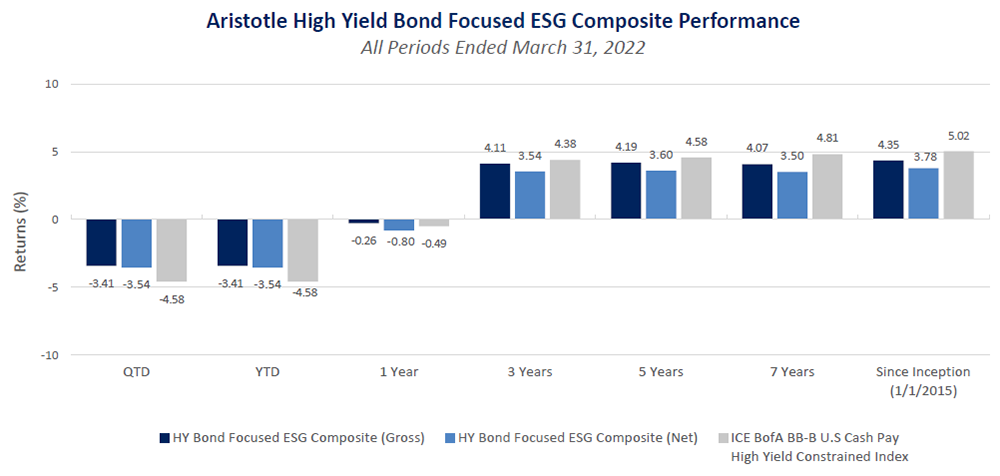

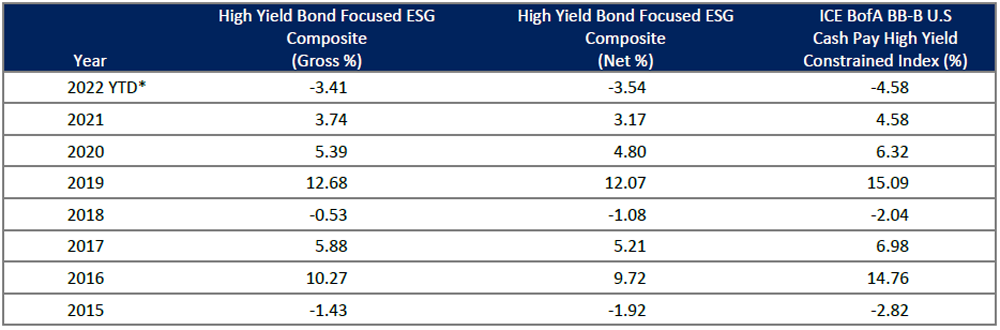

High Yield Bond Focused ESG

The Aristotle High Yield Bond Focused ESG Composite returned -3.41% gross of fees (-3.54% net of fees) in the first quarter, outperforming the -4.58% return of the ICE BofA BB-B U.S. Cash Pay High Yield Constrained Index.

Security selection contributed to relative performance led by holdings in Media & Entertainment and Retailers & Restaurants. This was partially offset by security selection in Diversified Manufacturing & Construction Machinery and Telecommunications. Industry allocation also contributed modestly to relative performance led by an underweight in Food, Beverage & Tobacco and an overweight in Lodging & Leisure. This was partially offset by an overweight in Retailers & Restaurants and an underweight in Energy. Additionally, sector rotation contributed modestly to relative performance led by the allocation to cash, which was partially offset by the allocation to investment grade corporate bonds.

| Top Five Contributors | Top Five Detractors |

|---|---|

| Quad/Graphics | Telecom Italia |

| Murphy Oil | Dell |

| Kraft Heinz | Scotts Miracle-Gro |

| iHeartMedia | United Rentals |

| Macy’s | Air Lease |

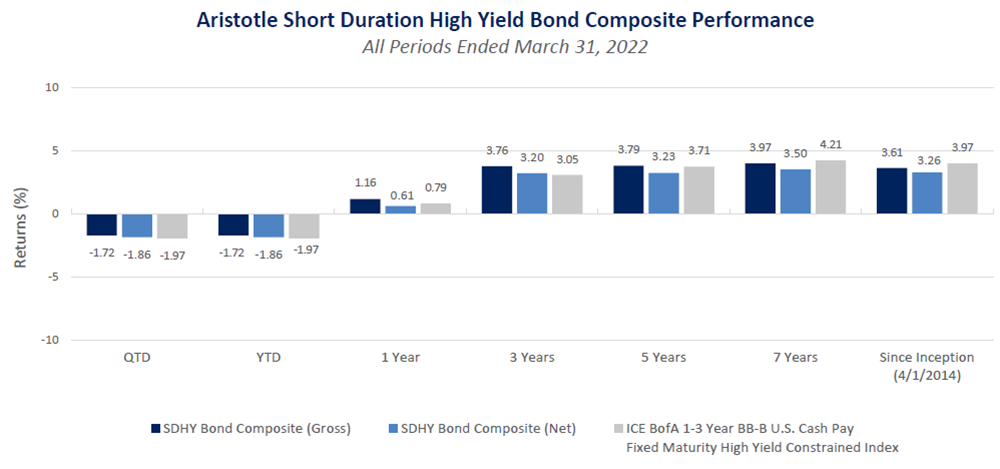

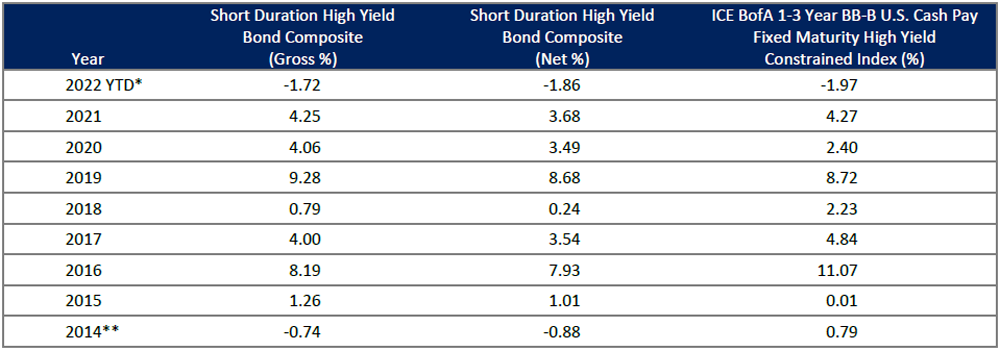

Short Duration High Yield Bond

The Aristotle Short Duration High Yield Bond Composite returned -1.72% gross of fees (-1.86% net of fees) in the first quarter, outperforming the -1.97% return of the ICE BofA 1-3 Year BB-B U.S. Cash Pay Fixed Maturity High Yield Constrained Index. Security selection was the primary contributor to relative performance, while industry allocation was the primary detractor from relative performance.

Security selection contributed to relative performance led by holdings in Chemicals and Healthcare. This was partially offset by security selection in Finance Companies and Lodging & Leisure. Sector rotation also contributed modestly to relative performance led by the allocation to cash, which was partially offset by the allocation to investment grade corporate bonds.

Industry allocation detracted modestly from relative performance led by an overweight in Chemicals and an underweight in Paper & Packaging. This was partially offset by an overweight in Media & Entertainment and an underweight in Technology.

| Top Five Contributors | Top Five Detractors |

|---|---|

| Uralkali PJSC | Equitrans Midstream |

| Murphy Oil | Royal Carribbean |

| Intesa Sanpaolo | Service Properties Trust |

| Delta Air Lines | MGM Resorts |

| Macy’s | Citgo |

Outlook

We believe three major themes have shaped the performance of corporate credit markets thus far in 2022: A more hawkish Fed, more persistent and higher-than-expected inflation and increased geopolitical risk resulting from Russia’s invasion of Ukraine. Despite the increase in uncertainty generated by these three themes, we continue to believe there are opportunities in U.S. corporate credit markets and maintain a positive outlook, especially for shorter duration high yield bonds.

The overall global macroeconomic backdrop has become significantly cloudier than it was at the end of 2021. While the Fed telegraphed tighter policy toward the end of last year, the Fed’s hawkishness so far in 2022 has caught the market by surprise and led to a rapid selloff, concentrated in the front end of the yield curve. With the Fed signaling quantitative tightening will begin in June, we believe there is the potential for the yield curve to steepen given the backdrop of a still strong economy and the extent of the repricing that has already occurred in the front end of the yield curve.

We also believe inflation risks could prove to be more stubborn than originally forecasted toward the end of last year. The impact of the war in Ukraine on commodity prices is just one example of how exogenous shocks have only magnified issues that could lead to stickier inflation. We believe consumers are already beginning to adapt their behavior to higher inflation, and the resulting rise in consumer inflation expectations could lead to more endemic inflation. In our opinion, there is a possibility that companies could eventually face a slowdown in topline demand as consumers’ discretionary income comes under pressure. For companies, the resulting pressure on margins and pricing power could push them to seek topline growth through more leveraged, shareholder-friendly policies.

High yield supply decreased more than we originally expected in the first quarter, and we believe issuance may continue to fall below expectations over the next few quarters. In our opinion, the opportunistic refinancing window for corporates is closed, thus the issuance that does occur this year could be used to fund share repurchases and mergers and acquisitions (M&A). We believe a shift from refinancing-related issuance to M&A and share repurchase-related issuance would be negative for credit market fundamentals. In the investment grade market, we also expect issuance to slow down, which would be positive on the margin for the supply/demand picture.

We believe overall risk, from geopolitical to credit risk, has increased significantly over the past three months. While we see these risks persisting in the coming quarters, we believe the best strategy to protect against these risks is to focus on credit fundamentals and segments of the market that, in our opinion, have already priced in what we believe to be a significant amount of risk, while seeking to avoid the segments of the market that could succumb to less balance sheet-friendly activities.

High Yield Bond Positioning

In our high yield bond portfolios, we continue to favor short duration high yield bonds, especially after the rapid repricing of the 2- to 3-year segment of the yield curve over the past quarter. From an industry perspective, we adjusted our portfolios to add exposure to companies that focus on providing consumer experiences rather than consumer goods.

While duration and interest rates are typically inversely correlated, duration has increased for many high yield bond benchmarks over the past quarter despite the large backup in U.S. yields. Before the increase in interest rates, many bonds had been trading to their call date but as interest rates have increased, these bonds are now trading to their maturity date. We believe most of this adjustment has already happened, and we continue to hold a duration underweight relative to the benchmark in our high yield bond portfolios.

With the reopening of the economy, we also believe there is pent-up demand for consumer experiences (e.g., travel and concerts), which could benefit companies in certain industries. Despite rising input costs, we believe some of the areas that may benefit are concert and event providers, conference-oriented lodging providers and airlines. As a result, we increased exposure to these areas, holding overweights in Media & Entertainment, Transportation and Lodging & Leisure alongside underweights in Technology, Telecommunications and Healthcare.

The opinions expressed herein are those of Aristotle Credit Partners, LLC (Aristotle Credit) and are subject to change without notice. Past performance is not a guarantee or indicator of future results. This material is not financial advice or an offer to buy or sell any product. You should not assume that any of the securities transactions, sectors or holdings discussed in this report are or will be profitable, or that recommendations Aristotle Credit makes in the future will be profitable or equal the performance of the securities listed in this report. The portfolio characteristics shown relate to the Aristotle Credit High Yield Bond – SMA strategy, the Aristotle Credit High Yield Bond Focused ESG strategy and the Aristotle Credit Short Duration High Yield Bond strategy. Not every client’s account will have these characteristics. Aristotle Credit reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and, in the aggregate, may represent only a small percentage of an account’s portfolio holdings. For a full list of all recommendations made by Aristotle Credit during the last 12 months, please contact us at (949) 681-2100. This is not a recommendation to buy or sell a particular security.

Returns are presented gross and net of investment advisory fees and include the reinvestment of all income. Gross returns will be reduced by fees and other expenses that may be incurred in the management of the account. For example, a 0.5% annual fee deducted quarterly (0.125%) from an account with a ten-year annualized growth rate of 5.0% will produce a net result of 4.4%. Actual performance results will vary from this example.

The Bloomberg U.S. Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes securities publicly issued by U.S. and non-U.S. industrial, utility and financial issuers that are all U.S. dollar denominated. The Bloomberg U.S. Corporate Bond Index is a component of the Bloomberg U.S. Credit Bond Index. The Bloomberg U.S. Corporate High Yield Bond Index measures the U.S. dollar-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on Bloomberg EM country definition, are excluded. The Credit Suisse Leveraged Loan Index is a market-weighted index designed to track the performance of the investable universe of the U.S. dollar-denominated leveraged loan market. The Bloomberg U.S. Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Index is frequently used as a stand-in for measuring the performance of the U.S. bond market. In addition to investment grade corporate debt, the Index tracks government debt, mortgage-backed securities (MBS) and asset-backed securities (ABS) to simulate the universe of investable bonds that meet certain criteria. In order to be included in the Index, bonds must be of investment grade or higher, have an outstanding par value of at least $100 million and have at least one year until maturity. The S&P 500 Index is the Standard & Poor’s Composite Index and is a widely recognized, unmanaged index of common stock prices. It is market cap weighted and includes 500 leading companies, capturing approximately 80% coverage of available market capitalization. The ICE Bank of America (ICE BofA) BB-B U.S. Cash Pay High Yield Constrained Index measures the performance of the U.S. dollar-denominated BB-rated and B-rated corporate debt issued in the U.S. domestic market, a fixed coupon schedule and a minimum amount outstanding of $100 million, issued publicly. Allocations to an individual issuer in the Index will not exceed 2%. The ICE Bank of America (ICE BofA) 1-3 Year BB-B U.S. Cash Pay Fixed Maturity High Yield Constrained Index tracks the performance of the U.S. dollar-denominated below investment grade corporate debt, currently in a coupon paying period, that is publicly issued in the U.S. domestic market; including 144A securities, both with and without registration rights. Qualifying securities must have risk exposure to countries are members of the FX-G10, Western Europe, or territories of the United States and Western Europe. The FX-G10 includes all Euro members: the United States, Japan, the United Kingdom, Canada, Australia, New Zealand, Switzerland, Norway and Sweden. Qualifying securities include only those rated BB1 through B3. Perpetual securities are not included as all securities must have a fixed final maturity date. All final maturity dates must range between one and three years. It is a capitalization-weighted index, constrained to 2% maximum weighting per issuer. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. The volatility (beta) of the Composites may be greater or less than the indices. It is not possible to invest directly in these indices. Composite and index returns reflect the reinvestment of income.

This presentation is to report on the investment strategies as reported by Aristotle Capital Management, LLC and is for illustrative purposes only. The information contained herein is obtained from multiple sources and believed to be reliable. Information has not been verified by Morgan Stanley Wealth Management, and may differ from documents created by Morgan Stanley Wealth Management. The financial advisor should refer to the Profile. This must be preceded or accompanied by the Morgan Stanley Wealth Management Profile, which you can obtain from the Morgan Stanley Wealth Management Performance Analytics. For additional information on other programs, please speak to Patrick Schussman at Aristotle Capital at (310) 954-8156.

Aristotle Credit Partners, LLC is an independent registered investment adviser under the Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Aristotle Credit, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request. ACP-2204-14-MSFA

Sources: SS&C Advent; ICE BofA

*Composite returns are preliminary pending final account reconciliation.

**2014 is a partial-year period of eleven months, representing data from February 1, 2014 to December 31, 2014.

Past performance is not indicative of future results. Returns presented are gross and net of investment advisory fees and include the reinvestment of all income. Please refer to disclosures at the end of this document.

Sources: SS&C Advent; ICE BofA

*Composite returns are preliminary pending final account reconciliation.

Past performance is not indicative of future results. Returns presented are gross and net of investment advisory fees and include the reinvestment of all income. Please refer to disclosures at the end of this document.

Sources: SS&C Advent; ICE BofA

*Composite returns are preliminary pending final account reconciliation.

**2014 is a partial-year period of period of nine months, representing data from April 1, 2014 to December 31, 2014.

Past performance is not indicative of future results. Returns presented are gross and net of investment advisory fees and include the reinvestment ofall income. Please refer to disclosures at the end of this document.