Commentary

Global Equity Advisory 4Q 2025

(All MSCI index returns are shown net and in U.S. dollars unless otherwise noted.)

Markets Review

Sources: CAPS CompositeHubTM, Bloomberg

Past performance is not indicative of future results. Aristotle Global Equity WM Composite returns are presented pure gross and net of maximum wrap fee and include the reinvestment of all income. Pure gross returns do not reflect the deduction of any trading costs or other fees and are supplemental to the net returns. Net returns are calculated by subtracting the highest applicable wrap/SMA fee, which includes trading costs and custodial fees, from the pure gross composite return. The highest applicable wrap/SMA fee is 2.00% on an annual basis, or 0.50% quarterly from inception to 12/31/2023 and 0.17% monthly from 1/1/2024 to present. Aristotle Capital Composite returns are preliminary pending final account reconciliation. Please see important disclosures at the end of this document.

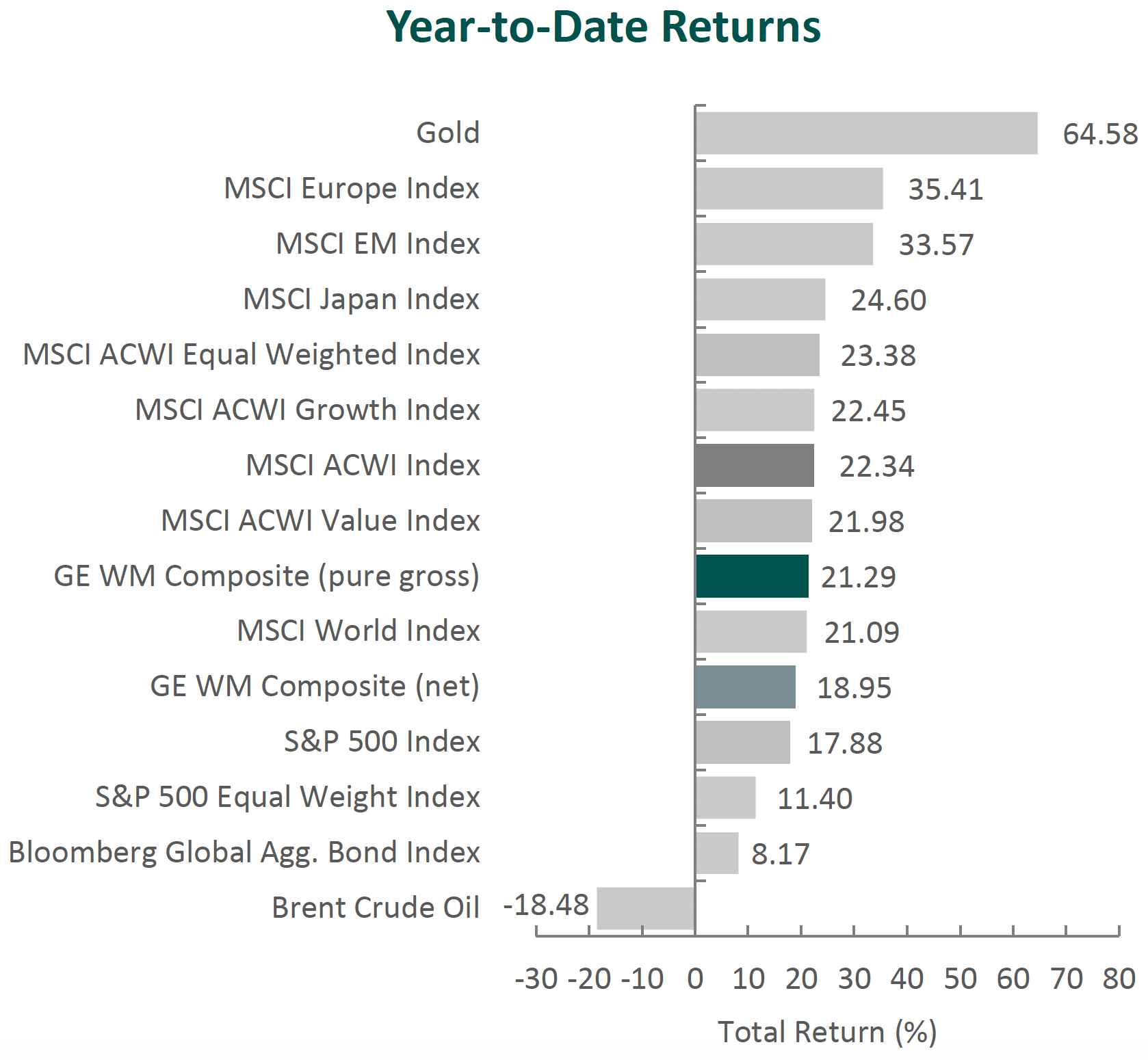

Global equity markets posted strong gains in the fourth quarter. The MSCI ACWI Index returned 3.29%, while bonds advanced in tandem (the Bloomberg Global Aggregate Bond Index increased 0.24%). Value stocks outperformed growth during the quarter, with the MSCI ACWI Value Index exceeding the MSCI ACWI Growth Index by 0.82%.

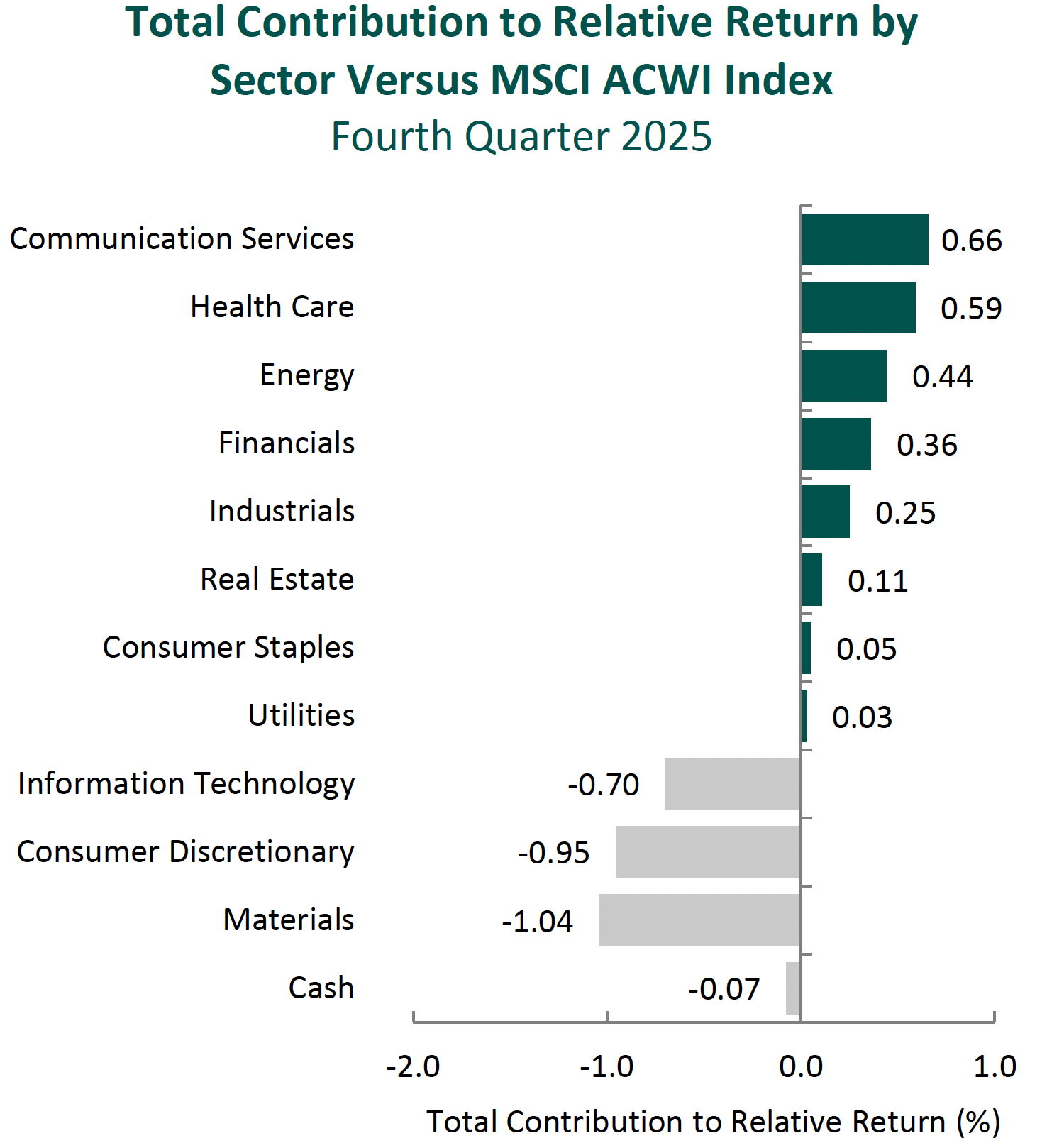

Gains in the global equity markets were broad-based during the period, with Latin America and Europe performing especially well, while gains in Africa & Middle East and North America were more subdued. On a sector basis, nine out of the eleven sectors within the MSCI ACWI Index advanced, led by Health Care, Materials and Financials. Real Estate, Consumer Discretionary and Consumer Staples were the worst-performing sectors.

On the whole, the macroeconomic outlook continued to gradually improve in late 2025. The IMF modestly upgraded its 2025 forecast for global GDP growth to 3.2%, citing resilience in many economies. However, growth is expected to decelerate in 2026 as the world economy adjusts to the cumulative impact of new policies (such as higher tariffs and industrial policies) and as one-off boosts fade. Temporary factors that propped up activity in 2025—for example, the front-loading of imports to get ahead of tariff changes and the reconfiguration of supply chains—are likely to wane. The IMF also warned that near-term risks are tilted to the downside. Key concerns include the sustainability of the AI-driven boom (fears of a potential bubble or abrupt repricing), persistent economic struggles in China, and increased fiscal vulnerabilities in many countries (which could pressure central banks). Policymakers have been urged to shore up confidence with credible, transparent strategies, such as rebuilding fiscal buffers and preserving central bank independence.

The U.S. economy continued to demonstrate resilience. Data released during the period showed that real GDP surged at a 4.3% annualized rate in the third quarter—the fastest quarterly growth in two years—driven primarily by robust consumer spending, with additional contributions from rising exports and increased government outlays. Despite this strength, consumer confidence deteriorated toward year-end; economists projected a moderation in spending, and concerns about the labor market persisted. The unemployment rate ticked up to 4.6% in November (a four-year high), though this level remains low by historical standards and is still consistent with an economy operating near full employment. Meanwhile, inflation moderated—the Consumer Price Index was up just 2.7% year-over-year in November, reaching its lowest level since July. Economists cautioned that recent unemployment and inflation figures were likely skewed by technical factors related to the 43-day government shutdown, which disrupted data reporting. This shutdown—the longest in U.S. history—forced approximately 1.4 million federal employees to go without pay and even led to temporary layoffs at some agencies before Congress passed a continuing resolution to reopen on November 12.

Given the mixed economic signals and uncertainty around the data, the Federal Reserve took a cautious stance. The Fed implemented two 0.25% interest rate cuts during the quarter, lowering the federal funds target range to 3.50%-3.75%. Fed Chair Powell emphasized a data-dependent approach, acknowledging risks to both sides of the Fed’s dual mandate. He noted the need to carefully assess incoming information, highlighting that policy would remain cautious and measured going into 2026.

Trade relations between the U.S. and China remained a key focus for markets. Early in the fourth quarter, tensions flared with tariff escalations and export controls. (China had dramatically expanded export controls on rare earth minerals, and the U.S. threatened 100% tariffs in retaliation.) Ultimately, President Trump and President Xi met at the Asia-Pacific Economic Cooperation (APEC) summit in South Korea and reached a one-year trade truce.

Corporate earnings remained robust. S&P 500 companies reported earnings growth of 13.6%, marking the fourth consecutive quarter of double-digit expansion. Of the 11 sectors within the S&P 500 Index, Information Technology recorded the strongest earnings growth of 29%. Artificial intelligence continued to be a major theme—more than 300 S&P 500 companies mentioned “AI” on their earnings calls during the fall. This enthusiasm helped propel mega-cap tech stocks higher and drive the market’s gains. However, as the quarter progressed, scrutiny increased around AI-related revenue circularity (companies buying AI services from each other to boost sales), the massive scale of AI-related capital spending, and the durability of longer-term returns on investment.

Annual Markets Review

Global equity markets continued their upward trajectory in 2025, with the MSCI ACWI delivering a full-year return of 22.34%. Growth stocks outperformed value during the year, as the MSCI ACWI Growth Index exceeded the MSCI ACWI Value Index by 0.47%. Meanwhile, fixed income markets rallied, as the Bloomberg Global Aggregate Bond Index advanced 8.17%.

As markets digested new trade agreements, economic data and policy decisions by central banks, 2025 proved to be a resilient year for risk assets. However, even strong markets presented their own set of challenges. Factors such as momentum and volatility outperformed quality, and while economic indicators and corporate earnings were broadly supportive, central banks and corporate management teams struck a more cautious tone heading into 2026.

Given the risks and uncertainties surrounding macroeconomic conditions and market narratives, we believe it remains prudent to focus on individual businesses and their long-term fundamentals. By concentrating on what is analyzable, we believe our approach is well suited to navigating a range of market environments while remaining disciplined through full market cycles.

Performance and Attribution Summary

For the fourth quarter of 2025, Aristotle Capital’s Global Equity WM Composite posted a total return of 3.87% pure gross of fees (3.37% net of fees), outperforming the MSCI ACWI Index, which returned 3.29%, and the MSCI World Index, which returned 3.12%. Please refer to the table below for detailed performance.

| Performance (%) | 4Q25 | 1 Year | 3 Years | 5 Years | 10 Years | Since Inception* |

|---|---|---|---|---|---|---|

| Global Equity WM Composite (pure gross) | 3.87 | 21.29 | 14.95 | 8.82 | 11.45 | 10.45 |

| Global Equity WM Composite (net) | 3.37 | 18.95 | 12.71 | 6.67 | 9.25 | 8.26 |

| MSCI ACWI Index (net) | 3.29 | 22.34 | 20.65 | 11.19 | 11.72 | 10.27 |

| MSCI World Index (net) | 3.12 | 21.09 | 21.17 | 12.15 | 12.17 | 11.08 |

Source: FactSet

Past performance is not indicative of future results. Sector attribution shows how much of a portfolio’s overall return is directly attributable to stock selection and asset allocation decisions within the portfolio, highlighting which sectors contributed or detracted to the total return. Attribution includes the reinvestment of income. Attribution is presented gross of fees and does not include the deduction of all fees and expenses that a client or investor has paid or would have paid. Please refer to the gross and net composite returns included within to understand the overall impact of fees.

From a sector perspective, the portfolio’s performance relative to the MSCI ACWI Index can be attributed to allocation effects, while security selection detracted. Security selection in Communication Services, Energy, and Health Care contributed the most to the portfolio’s relative performance. Conversely, security selection in Materials, Consumer Discretionary and Information Technology detracted from relative return.

Regionally, allocation effects were responsible for the portfolio’s performance relative to the MSCI ACWI Index, while security selection detracted. Security selection in Asia/Pacific ex-Japan contributed the most to relative performance, while security selection in North America was the largest detractor.

Contributors and Detractors for 4Q 2025

| Relative Contributors | Relative Detractors |

|---|---|

| Jazz Pharmaceuticals | Lennar |

| Erste Group Bank | Nemetschek |

| FANUC | Uber |

| LVMH Moët Hennessy Louis Vuitton | Sony |

| Cameco | FMC |

Erste Group Bank, a leading retail and commercial bank in Central and Eastern Europe, was a primary contributor during the quarter. The company reported strong operating performance, driven by healthy loan growth across core markets, resilient net interest income and solid fee income, with contributions from securities, asset management and payments. Its diversified, retail-oriented banking model, leading market positions across core geographies and strong deposit franchise anchored in household customers continue to support the business. During the quarter, Erste cleared key milestones related to its previously announced acquisition of a 49% stake in Santander Bank Polska. With regulatory conditions satisfied late in the quarter, the transaction is expected to close in early 2026. We view this transaction as strategically attractive, expanding Erste’s footprint into Poland, one of the region’s largest and most dynamic banking markets, while enhancing scale and diversification. More broadly, Erste’s exposure to underbanked Central and Eastern European economies positions the company to benefit as incomes rise and demand for credit, savings and financial services continues to grow. Ongoing investment in technology and digital capabilities supports efficiency, customer engagement and long-term profitability.

FANUC, the Japanese leader in factory automation and industrial robotics, was a top contributor during the quarter. The company operates across factory automation systems, industrial robots and precision machining centers, serving automotive, electronics and general industrial end markets. Results through the first half of fiscal year 2025 marked a clear inflection, with operating margin expanding to 21% as factory utilization and pricing discipline held firm. Performance was further supported by a sharp rebound in China, where robot sales grew over 80% year-over-year, more than offsetting softer demand in Europe and Japan. Beyond the cyclical recovery, FANUC continues to deepen its competitive advantages. Its dominant position in computer numerical control (CNC) systems, the “brains” of machine tools, underpins a large and highly sticky installed base. During the quarter, the company highlighted an increasingly open software strategy that allows third parties to develop applications directly on FANUC’s platform while maintaining safety and reliability at the controller level. This approach is reinforced by FANUC’s collaboration with NVIDIA, announced during the quarter and linking FANUC’s robot simulation tools with NVIDIA’s Omniverse software to enable highly accurate digital twins and accelerate deployment of AI-driven robotics. This leadership extends across its Robot and Robomachine segments, supported by an integrated hardware, software and service ecosystem that is difficult to replicate and highly valued in mission-critical applications. As global automation adoption accelerates amid labor shortages, rising wages and increasing manufacturing complexity, we believe FANUC is well-positioned to grow alongside its customers while sustaining attractive margins, supported by disciplined capital allocation and a growing mix of higher-margin service and software revenues.

Uber, a leading rideshare, delivery and shipping technology platform, was one of the largest detractors during the period. Trip volumes reached record levels, and gross bookings grew significantly year-over-year, yet the stock underperformed as investor focus shifted from growth to margin trajectory, regulatory risk and autonomous vehicle (AV) uncertainty. The primary near-term concern among market participants was management’s guidance around profitability. While results exceeded expectations on bookings and FREE cash flow, Uber signaled a deliberate moderation in margin expansion, as incremental profits are reinvested into affordability, cross-platform engagement and early AV initiatives. Regulatory concerns also resurfaced, particularly in Europe, where ongoing debates around driver classification and data protection continue to pose potential cost (and therefore margin) headwinds. At the same time, competitive anxiety around AVs intensified following Lyft’s expanded partnership with Waymo and continued investor focus on Tesla’s long-term robotaxi ambitions. Management acknowledged that autonomous initiatives will pressure near-term margins, as Uber invests to build supply and data infrastructure, even as utilization in early AV markets has been encouraging. Over the long term, however, our thesis remains intact. Uber’s global scale, deepening network effects, growing FREE cash flow and expanding cross-platform ecosystem position the company to compound value as profitability improves and new mobility technologies mature.

Sony, the global leader in video games, image sensors, music and movies, was a primary detractor for the period. Shares declined following the recognition of a one-time, non-cash charge of approximately ¥50 billion in the Game & Network Services segment related to an impairment and accounting correction of previously capitalized development costs. Importantly, this charge was not recurring and did not reflect a deterioration in underlying operating performance. Excluding this item, operating income would have increased approximately 23% year-over-year, supported by healthy gaming engagement, continued growth in network services and software sales, and strong results in the Music segment driven by streaming growth and recent theatrical releases. The company’s image sensor business also benefited from a favorable product mix and steady end-market demand. Looking ahead, we continue to see opportunity for Sony to capitalize on its unique position as both a content creator and platform owner. The company’s ability to integrate gaming, music, anime and film—and to leverage IP across its ecosystem—supports sustained engagement and recurring revenue. In addition, the recent spinoff of Sony’s Financial Services segment further sharpens management’s focus on its core content, technology and entertainment operations. We believe Sony’s industry leadership and continued focus on operational execution position the company well for long-term value creation.

Recent Portfolio Activity

| Buys | Sells |

|---|---|

| Itochu | FMC |

| Lowe’s | Nidec |

During the quarter, we sold our positions in FMC and Nidec and purchased Itochu and Lowe’s.

We initially invested in FMC, one of the world’s largest patented crop protection companies, in the first quarter of 2022. We were attracted to FMC’s position as a focused, pure-play agricultural chemicals business following its acquisition of DuPont’s crop protection portfolio and the divestiture of its lithium business. These actions resulted in a differentiated portfolio supported by patents and niche products, as well as a deep research pipeline and an experienced management team. The position recently underwent a sale review, prompted by a combination of stock price underperformance, patent expirations and a prolonged industry downturn. Management’s restructuring efforts included an exit from India, which necessitated FMC to temporarily repurchase inventory in that country. This action, combined with a reduced earnings outlook in the company’s Latin American operations, resulted in materially lower cash flow guidance and reduced balance sheet flexibility. Taken together, these factors raised the risk profile of the investment beyond our expectations. As a result, we exited the position and redeployed the proceeds into what we believe is a more attractive opportunity.

We invested in Nidec more than a decade ago, initially attracted by the company’s position as a global leader in precision motors, its strong market share across hard disk drive, its growing presence in industrial and automotive applications, and its ability to consolidate a fragmented industry while generating attractive margins and returns on invested capital. Over our holding period, Nidec maintained leadership in several core motor categories and benefited from long-term demand for energy-efficient solutions across industrial, appliance and data center markets. However, several anticipated catalysts were slower to materialize. The company’s expansion into electric vehicle traction motors proved more competitive and less profitable than expected, while frequent leadership changes, strategic shifts and, more recently, manufacturing and accounting issues introduced persistent uncertainty. Despite efforts to improve discipline and profitability, ongoing investigations and questions around business quality and controls reduced the clarity and predictability of the business. Given these unresolved issues, we concluded that Nidec no longer offered an attractive risk-adjusted return and exited the position.

Itochu Corporation

Headquartered in Osaka, Japan and founded in 1858, Itochu is one of Japan’s largest general trading companies, known as sogo shosha. These diversified conglomerates combine global trading, investment and operating businesses across a wide range of industries. They play a central role in Japan’s economy by facilitating supply chains, allocating capital and operating businesses both domestically and internationally. Itochu’s portfolio spans consumer, industrial and selective resource businesses and is supported by a long-standing global operating network.

High-Quality Business

Some of the quality characteristics we have identified for Itochu include:

- A differentiated business mix with a greater emphasis on non-resource and consumer-facing businesses relative to other Japanese trading houses, contributing to more stable earnings and returns across cycles;

- Strong competitive positioning across several operating subsidiaries and affiliates, including leading brands and platforms such as FamilyMart, Descente, and Tokyo Century, which benefit from scale, brand strength and operational expertise; and

- A disciplined approach to capital allocation, including active asset recycling, a willingness to restructure or exit underperforming businesses, and a consistent focus on maintaining returns on invested capital above the cost of capital.

Attractive Valuation

We believe shares of Itochu are attractively valued relative to the quality and durability of its business. Given the breadth of businesses within Itochu’s portfolio, we believe the market does not fully reflect the earnings potential and capital return opportunities embedded across its operations.

Compelling Catalysts

Catalysts we have identified for Itochu, which we believe will cause its stock price to appreciate over our three- to five-year investment horizon, include:

- Higher normalized earnings from non-resource businesses, particularly in food, retail and consumer-related segments, helping to moderate volatility from commodity-exposed activities;

- Continued improvements in capital efficiency and shareholder returns through a combination of dividend growth and share repurchases; and

- Ongoing portfolio management initiatives, including asset recycling and increased ownership in higher-quality subsidiaries, which we believe can enhance returns and simplify the business over time.

Lowe’s Companies, Inc.

Founded in 1921 and headquartered in Mooresville, North Carolina, Lowe’s is the world’s second-largest home improvement retailer, behind Home Depot. The company operates more than 1,700 stores across the United States, offering a broad assortment of products used in home maintenance, repair, remodeling and improvement, ranging from appliances and hardware to décor and outdoor products.

Lowe’s stores are typically located in suburban markets and primarily serve retail “do-it-yourself” (DIY) customers, which account for roughly 70% of revenue. More than 60% of sales are tied to home maintenance and repair activity. This contrasts with Home Depot’s more metropolitan store footprint and greater exposure to professional customers. We had previously been investors in Home Depot. While Home Depot executed more effectively over much of the past decade, particularly in serving large professional customers and improving store productivity, we believe Lowe’s has begun to narrow this gap following the appointment of Marvin Ellison as CEO in 2018. Drawing on his expertise at Home Depot, management has initiated a multi-year transformation focused on operational discipline, productivity and improved customer service.

High-Quality Business

Some of the quality characteristics we have identified for Lowe’s include:

- Meaningful economies of scale, supported by an extensive store network, which provide cost advantages and significant purchasing power with vendors and suppliers;

- A differentiated in-store experience driven by the product knowledge and expertise of Lowe’s associates, contributing to the company’s ~10% share of a highly fragmented home improvement market;

- Structural resilience to e-commerce disruption, as many home improvement products are either bulky, costly to ship or required on short notice, limiting the threat from online-only competitors (i.e., Amazon); and

- Strong brand recognition and a one-stop-shop value proposition that reinforces customer loyalty and creates a self-reinforcing scale advantage over time.

Attractive Valuation

We believe shares of Lowe’s are attractively valued relative to our estimates of normalized earnings. In our view, the market underappreciates Lowe’s opportunity to gain market share, particularly with professional customers, and to improve profitability through enhanced store efficiency, supply chain optimization and digital capabilities.

Compelling Catalysts

Catalysts we have identified for Lowe’s, which we believe can drive stock price appreciation over our three- to five-year investment horizon include:

- Market share gains driven by improvements to supply-chain infrastructure, upgraded IT systems and enhanced omnichannel capabilities, including “buy online, pick up in-store” offerings;

- Increased penetration with professional customers as the company refocuses on products, service levels and capabilities tailored to this higher-value segment, which generates significantly more annual store visits and spend than DIY customers; and

- Rising sales per square foot and operating margins as Lowe’s shifts its strategic focus away from store expansion and toward improving productivity and returns within its existing store base.

Conclusion

Markets and economic conditions will continue to evolve, often in ways that are difficult to anticipate. While we remain attentive to these developments, our work is ultimately centered on understanding individual businesses—how they compete, how they allocate capital and how their economics change over time. We recognize that progress in business fundamentals and investment outcomes do not always align over shorter periods. Thus, we approach our investment process with patience and a willingness to reassess our views as circumstances change. Rather than react impulsively to every macro headline or try to time short-term market moves, we focus on what is analyzable and enduring: the long-term fundamentals of the companies we own. We believe this careful, fundamental approach remains the most reliable way to add value for our clients over the long run, across a wide range of market environments.

The opinions expressed herein are those of Aristotle Capital Management, LLC (Aristotle Capital) and are subject to change without notice. Past performance is not a guarantee or indicator of future results. This material is not financial advice or an offer to buy or sell any product. You should not assume that any of the securities transactions, sectors or holdings discussed in this report were or will be profitable, or that recommendations Aristotle Capital makes in the future will be profitable or equal the performance of the securities listed in this report. The portfolio characteristics shown relate to the Aristotle Global Equity Advisory strategy. Not every client’s account will have these characteristics. Aristotle Capital reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and, in the aggregate, may represent only a small percentage of an account’s portfolio holdings. The performance attribution presented is of a representative account from Aristotle Capital’s Global Equity WM Composite. The representative account is a discretionary client account which was chosen to most closely reflect the investment style of the strategy. The criteria used for representative account selection is based on the account’s period of time under management and its similarity of holdings in relation to the strategy. Recommendations made in the last 12 months are available upon request.

Composite returns are presented pure gross and net of the maximum wrap fee and include the reinvestment of all income. Pure gross returns do not reflect the deduction of any trading costs or other fees and are supplemental to the net returns. Net returns are calculated by subtracting the highest applicable wrap/SMA fee, which includes trading costs and custodial fees, from the pure gross composite return. The highest applicable wrap/SMA fee is 2.00% on an annual basis, or 0.50% quarterly from inception to 12/31/2023 and 0.17% monthly from 1/1/2024 to present.

All investments carry a certain degree of risk, including the possible loss of principal. Investments are also subject to political, market, currency and regulatory risks or economic developments. International investments involve special risks that may in particular cause a loss in principal, including currency fluctuation, lower liquidity, different accounting methods and economic and political systems, and higher transaction costs. These risks typically are greater in emerging markets. While Large-capitalization companies may have more stable prices than smaller, less established companies, they are still subject to equity securities risk. In addition, large-capitalization equity security prices may not rise as much as prices of equity securities of small-capitalization companies. Securities of small- and medium-sized companies tend to have a shorter history of operations and be more volatile and less liquid. Value stocks can perform differently from the market as a whole and other types of stocks. The material is provided for informational and/or educational purposes only and is not intended to be and should not be construed as investment, legal or tax advice and/or a legal opinion. Investors should consult their financial and tax adviser before making investments. The opinions referenced are as of the date of publication, may be modified due to changes in the market or economic conditions, and may not necessarily come to pass. Information and data presented has been developed internally and/or obtained from sources believed to be reliable. Aristotle Capital does not guarantee the accuracy, adequacy or completeness of such information.

Aristotle Capital Management, LLC is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Aristotle Capital, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request. ACM-2601-77

Sources: CAPS CompositeHubTM, MSCI

MSCI ACWI (Net) was stated as the primary benchmark on June 1, 2024 and MSCI World (Net) became the secondary benchmark.

The Aristotle Global Equity WM Composite has an inception date of December 1, 2010. As of 1/1/2024, the composite was renamed from the Global Equity Advisory Composite.

Past performance is not indicative of future results. The information provided should not be considered financial advice or a recommendation to purchase or sell any particular security or product. Performance results for periods greater than one year have been annualized.

Composite returns are presented pure gross and net of the maximum wrap fee and include the reinvestment of all income. Pure gross returns do not reflect the deduction of any trading costs or other fees and are supplemental to the net returns. Net returns are calculated by subtracting the highest applicable wrap/SMA fee, which includes trading costs and custodial fees, from the pure gross composite return. The highest applicable wrap/SMA fee is 2.00% on an annual basis, or 0.50% quarterly from inception to 12/31/2023 and 0.17% monthly from 1/1/2024 to present.

MSCI ACWI (Net) was stated as the primary benchmark on June 1, 2024 and MSCI World (Net) became the secondary benchmark. The MSCI ACWI captures large and mid-cap representation across 23 developed markets and 24 emerging markets countries. With approximately 2,500 constituents, the Index covers approximately 85% of the global investable equity opportunity set. The MSCI World Index consists of the following 23 developed market country indexes: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. The MSCI ACWI Equal Weighted Index represents an alternative weighting scheme to its market cap weighted parent index, MSCI ACWI. The Index includes the same constituents as its parent (large and mid-cap securities from 23 developed markets and 24 emerging markets countries. However, at each quarterly rebalance date, all index constituents are weighted equally, effectively removing the influence of each constituent’s current price (high or low). Between rebalances, index constituent weightings will fluctuate due to price performance. The MSCI Emerging Markets Index is a free float-adjusted market capitalization-weighted index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 24 emerging market country indexes: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates. The MSCI ACWI Growth Index captures large and mid-cap securities exhibiting overall growth style characteristics across 23 developed markets countries and 24 emerging markets countries. The MSCI ACWI Value Index captures large and mid-cap securities exhibiting overall value style characteristics across 23 developed markets countries and 24 emerging markets countries. The MSCI Europe Index captures large and mid-cap representation across 15 developed markets countries in Europe. With approximately 400 constituents, the Index covers approximately 85% of the free float-adjusted market capitalization across the European developed markets equity universe. The MSCI Japan Index is designed to measure the performance of the large and mid-cap segments of the Japanese market. With approximately 200 constituents, the Index covers approximately 85% of the free float-adjusted market capitalization in Japan. The S&P 500® Index is the Standard & Poor’s Composite Index of 500 stocks and is a widely recognized, unmanaged index of common stock prices. The S&P 500 Equal Weight Index is designed to be the size-neutral version of the S&P 500. It includes the same constituents as the cap-weighted S&P 500, but each company in the S&P 500 Equal Weight Index is allocated the same weight at each quarterly rebalance. The Bloomberg Global Aggregate Bond Index is a flagship measure of global investment grade debt from 27 local currency markets. This multi-currency benchmark includes Treasury, government-related, corporate and securitized fixed rate bonds from both developed and emerging markets issuers. The Brent Crude Oil Index is a major trading classification of sweet light crude oil that serves as a major benchmark price for purchases of oil worldwide. The U.S. Consumer Price Index is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. The volatility (beta) of the Composite may be greater or less than the benchmarks. It is not possible to invest directly in these indexes.