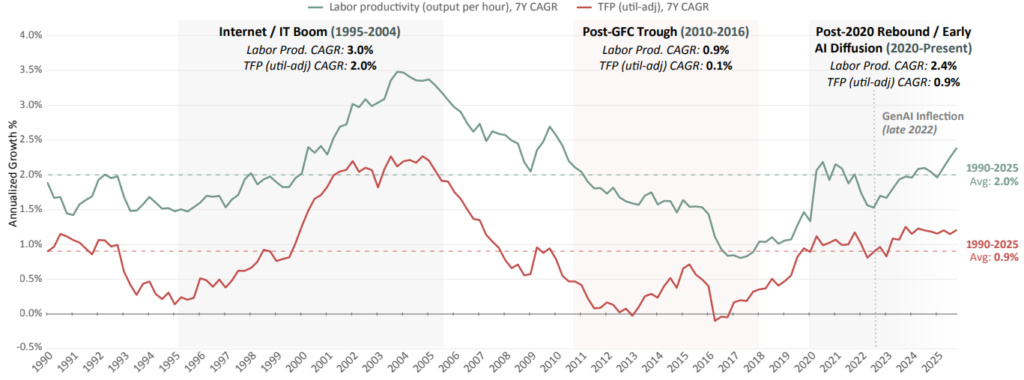

Chart Insights

Is the Productivity Cycle Turning?

Long-run productivity has historically moved in waves, and the current one may be inflecting.

Labor productivity (output per hour) is the headline measure, while utilization-adjusted total factor productivity (TFP) clarifies underlying efficiency, to distinguish true efficiency gains from temporary effects.

The 1995–2004 Internet and IT boom delivered broad based gains, with labor productivity ~3.0% CAGR and utilization-adjusted TFP CAGR ~2.0%.

Since 1990, productivity has moved in multi-year waves, peaking in the early-2000s and bottoming in the mid-2010s post-GFC trough.

Since 2020, labor productivity has reaccelerated above its long-term average; TFP has improved but remains well below prior highs, suggesting sustained TFP strength is needed for a durable AI-led shift.

Labor Productivity vs. TFP (7-year trailing CAGR): 1990-2025

Note: Lines show 7-year trailing CAGR. Shaded figures show period CAGR of the underlying level series.

Source: U.S. Bureau of Labor Statistics (BLS), Labor Productivity and Costs (Nonfarm Business Sector output per hour); Fernald, Federal Reserve Bank of San Francisco

(utilization-adjusted TFP); Aristotle Capital Management, author calculations. As of 2025Q4.

All investments carry a certain degree of risk, including the possible loss of principal. Investments are also subject to political, market, currency and regulatory risks or economic developments. International investments involve special risks that may in particular cause a loss in principal, including currency fluctuation, lower liquidity, different accounting methods and economic and political systems, and higher transaction costs. These risks typically are greater in emerging markets. While Large capitalization companies may have more stable prices than smaller, less established companies, they are still subject to equity securities risk. In addition, large-capitalization equity security prices may not rise as much as prices of equity securities of small-capitalization companies. Securities of small- and medium-sized companies tend to have a shorter history of operations, be more volatile and less liquid. Value stocks can perform differently from the market as a whole and other types of stocks. The material is provided for informational and/or educational purposes only and is not intended to be and should not be construed as investment, legal or tax advice and/or a legal opinion. Investors should consult their financial and tax adviser before making investments. The opinions referenced are as of the date of publication, may be modified due to changes in the market or economic conditions, and may not necessarily come to pass. Information and data presented has been developed internally and/or obtained from sources believed to be reliable. Aristotle Capital does not guarantee the accuracy, adequacy or completeness of such information.

Aristotle Capital Management, LLC (Aristotle Capital) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Aristotle Capital, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request. ACM-2603-122